Nvidia (NASDAQ: NVDA) has achieved astonishing progress over the previous 12 months. Graphics processing models (GPUs) are the new commodity for powering synthetic intelligence (AI) in knowledge facilities, and Nvidia has lengthy dominated the GPU market.

The shift to AI is driving a rise in knowledge middle investments, giving Nvidia a tailwind. The corporate expects first-quarter income to triple 12 months over 12 months to $24 billion, however wanting on the long-term outlook, there are two principal the explanation why this AI inventory nonetheless has room to run.

1. Development in AI infrastructure spending

Knowledge middle merchandise are Nvidia’s largest income. This section accounted for 83% of its $22 billion in income in the newest quarter, so the funding in knowledge middle infrastructure is vital to Nvidia’s progress.

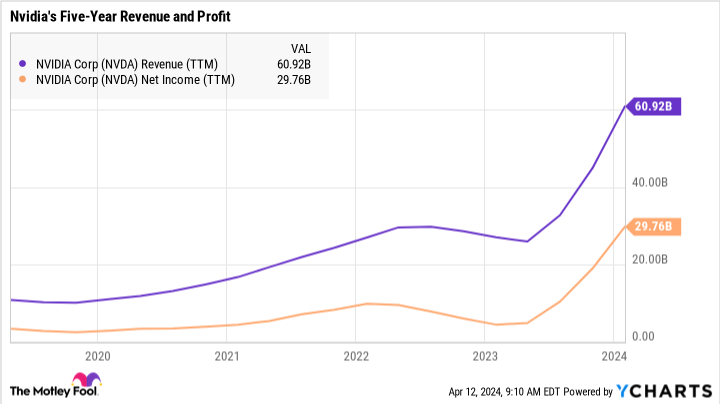

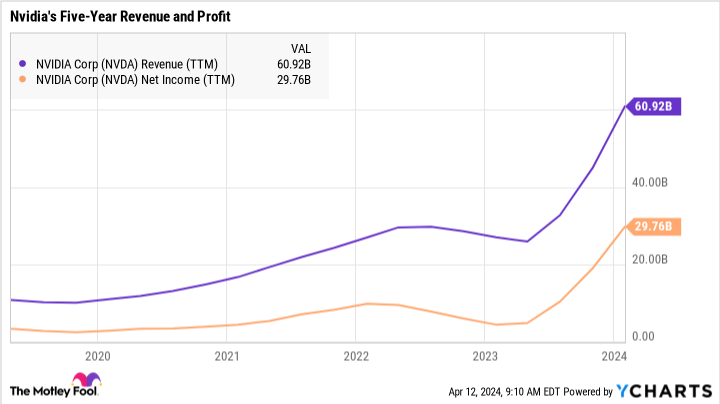

Based on Dell’Oro Group, knowledge middle spending by the highest 10 cloud service suppliers totaled $260 billion by 2023. AI-related spending is rising a lot sooner than the general knowledge middle market, and that is mirrored in Nvidia’s numbers. The corporate’s income greater than doubled final 12 months to just about $61 billion.

By 2024, Dell’Oro expects complete knowledge middle infrastructure spending to extend to 11%, pushed by investments to assist new purposes powered by generative AI. Different corporations level to excessive demand for Nvidia chips. Dell Applied sciencesan Nvidia buyer, mentioned its backlog of AI-optimized servers practically doubled in the newest quarter.

It’s necessary to do not forget that Nvidia affords extra than simply GPUs. It additionally supplies software program and techniques, which is a profitable alternative.

2. Nvidia will squeeze each ounce of revenue out of this chance

For all of the hype surrounding Nvidia’s industry-leading AI chips, the corporate doesn’t get sufficient credit score for the way in which it well positions its merchandise for worthwhile progress.

For years, Nvidia has positioned its gaming GPUs to allow will increase in common promoting costs as avid gamers moved to the newest graphics playing cards. This boosted income and generated good returns for shareholders. The corporate’s method to knowledge facilities can be geared toward producing excessive returns.

For instance, Nvidia doesn’t simply promote particular person chips to knowledge facilities; it bundles them right into a system. Nvidia’s DGX system contains eight H100 GPUs, that are individually fairly costly. The extra software program and companies that Nvidia affords on prime of its {hardware} add numerous worth that it may well monetize with excessive margins.

Nvidia’s web revenue grew 581% final 12 months to just about $30 billion, or virtually half of its complete income. The excessive revenue margin Nvidia generates from gross sales makes the inventory a strong long-term funding.

Nvidia will face competitors. Intel And Superior micro gadgets are already engaged on AI chips to compete with Nvidia, however Nvidia is the innovator in GPU expertise, and its latest progress spurt offers it an enormous benefit when it comes to monetary sources to take care of its lead within the GPU market to guard.

Analysts presently count on Nvidia to develop earnings per share by 35% yearly within the coming years. The inventory received’t proceed to double yearly, however with administration valuing the info middle alternative at $1 trillion, there’s loads of room for the inventory to succeed in new highs over the following decade.

Ought to You Make investments $1,000 in Nvidia Now?

Contemplate the next earlier than shopping for shares in Nvidia:

The Motley Idiot inventory advisor The analyst crew has simply recognized what they assume is the 10 finest shares for buyers to purchase now… and Nvidia wasn’t considered one of them. The ten shares that made the minimize might ship monster returns within the coming years.

Inventory Advisor supplies buyers with an easy-to-follow blueprint for achievement, together with portfolio constructing steerage, common analyst updates and two new inventory picks per thirty days. The Inventory Advisor service has greater than tripled the return of the S&P 500 since 2002*.

View the ten shares

*Inventory Advisor returns April 8, 2024

John Ballard has positions in Superior Micro Units and Nvidia. The Motley Idiot holds positions in and recommends Superior Micro Units and Nvidia. The Motley Idiot recommends Intel and recommends the next choices: lengthy January 2023 $57.50 calls on Intel, lengthy January 2025 $45 calls on Intel, and quick Could 2024 $47 calls on Intel. The Motley Idiot has a disclosure coverage.

2 Causes to Purchase Nvidia Inventory Like There’s No Tomorrow was initially revealed by The Motley Idiot