justocker

The Dominion Purchase Thesis

There’s a super unfold between the sentiment on Dominion Power, Inc. (NYSE:D) and its elementary ahead outlook. The market is approaching D with apprehension and buying and selling it at low multiples whereas the basics look strongly optimistic given the fast progress in power wants in Northern Virginia (NOVA) with D as the one main participant positioned to offer that power. The buildout of ample energy to gas the info middle increase in NOVA can gas regular progress for Dominion for the foreseeable future.

Allow us to start by discussing how D acquired so low cost and comply with with the demand drivers behind its future progress.

Why sentiment and pricing of Dominion inventory are so low

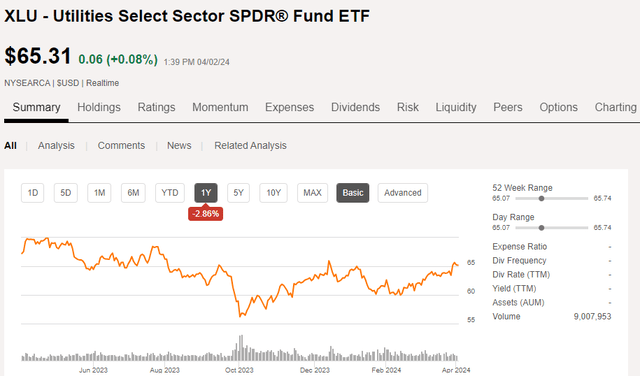

Utilities are usually not a preferred sector proper now. With the fast rise in rates of interest of the previous 2 years, there are lots of locations buyers can go to get funding earnings. This has displaced a good portion of the utility investor pool. They merely have extra competing choices. As such, the sector has suffered as measured by the Utilities Choose Sector SPDR Fund ETF (XLU).

SA

Dominion has fallen considerably additional because it dedicated the cardinal sin of slicing its dividend in a sector recognized for dividend stability. Frankly, most utility buyers simply aren’t fascinated with investing in an organization the place they do not really feel their earnings is secure. Earnings buyers bought and given the dearth of pleasure for the sector there have been only a few patrons to interchange them. The inventory needed to fall sufficiently far to get worth buyers .

SA

On the now worth worth, a ample quantum of latest curiosity has are available to kind a brand new market equilibrium.

At this worth level, I feel the general proposition of Dominion as a worth play, a progress play, and an earnings play is extraordinarily compelling.

Explosive electrical energy demand progress in Dominion’s core markets

Dominion is the first electrical utility serving a lot of Virginia, however notably a few key markets in Northern Virginia:

- Ashburn – also referred to as the info middle hub of the world.

- Loudoun County – the spillover information facilities that do not slot in Ashburn.

Ashburn has a low price of electrical energy and its proximity to Washington DC makes it a handy hub for information facilities. With the very best focus of knowledge facilities wherever on the earth, it has develop into an “all roads result in Rome” type of scenario. Main fiberoptic cable backbones path to NOVA which in flip makes it a good higher place to construct information facilities.

For many areas not on hubs, connectivity is slower. In Wisconsin, for instance, most alerts are usually not despatched on to me, however slightly get routed by means of the hub in Chicago, after which after I ship alerts again out in addition they are inclined to undergo Chicago. Oblique routes add milliseconds of latency which for the cloud computing in information facilities provides as much as be a giant deal. There are solely a handful of main fiber hubs on the earth and NOVA is the most important hub.

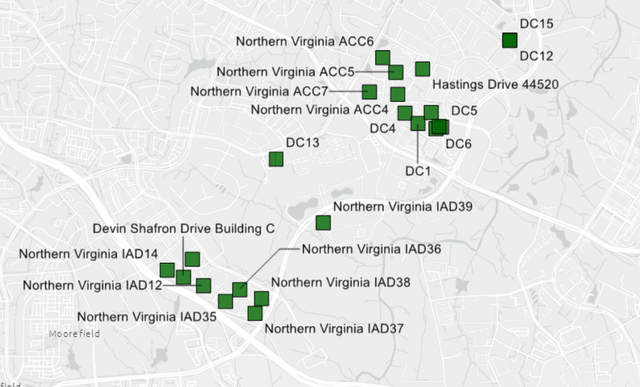

So whereas low cost electrical energy was maybe the start line of it turning into an information middle hub, its market-leading place is self-fulfilling. The info middle REITs have many information facilities in Ashburn with these of Digital Realty Belief, Inc. (DLR) and Equinix, Inc. (EQIX) mapped under.

S&P International Market Intelligence

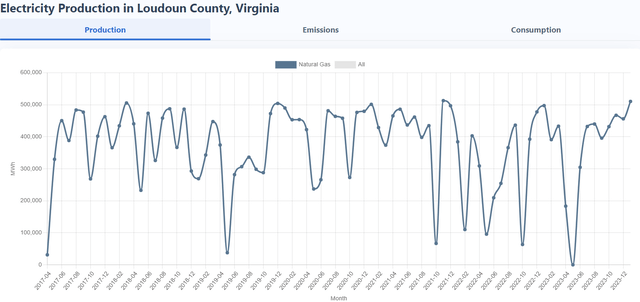

Information facilities are energy hungry. The fast progress of knowledge facilities in NOVA has brought about energy demand to overhaul the provision of energy. Electrical energy manufacturing has been pretty flat at roughly 300,000 to 400,000 MWh, smoothing out the bumps.

findenergy

Supply: FindEnergy: Energy Provider Facts and Statistics

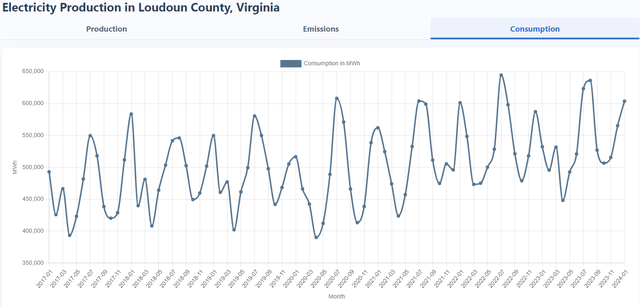

Demand, nonetheless, has been steadily growing, now averaging about 575,000 MWh.

findenergy

Supply: FindEnergy: Power Supplier Info and Statistics

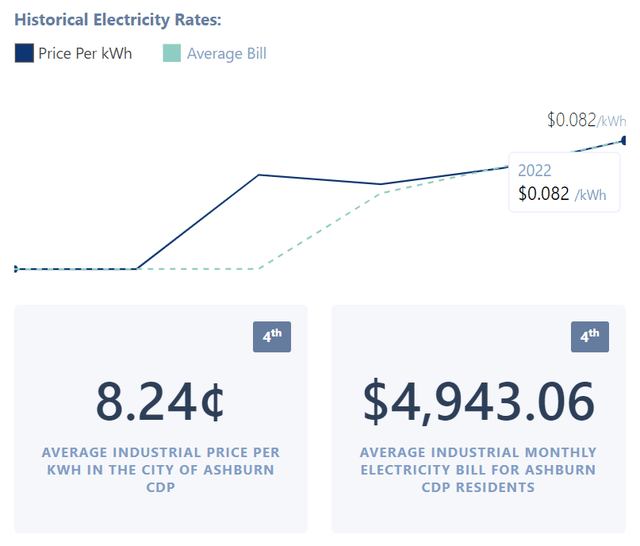

The result’s that power costs in Ashburn are going up for industrial customers.

findenergy

Findenergy.com

Demand for electrical energy continues to develop as extra information facilities are constructed. Yardi Matrix summarizes the info middle growth in NOVA.

“Northern Virginia, which has the very best focus of knowledge facilities within the nation, additionally has essentially the most new growth underway. The market has twice as a lot accomplished area as Dallas, the second-largest market, and the present infrastructure gives a bonus over different areas. Nevertheless, there are rising considerations about Northern Virginia’s capability so as to add extra information facilities as a result of huge quantity of energy required by the amenities. That is very true throughout an AI-fueled increase as a result of AI mannequin coaching requires power-hungry GPUs, utilizing an estimated two to 5 instances extra energy than an everyday cloud server”

That final bit is the place electrical energy demand progress may develop into explosive. Extra information facilities improve energy consumption linearly, however as information facilities change to GPU-based for synthetic intelligence functions, the facility calls for develop 2X to 5X.

This stacks multiplicatively. There are extra information facilities below growth and every information middle goes to demand increasingly more energy.

Electrical energy Demand Fueling Dominion’s Capital Funding

Dominion is the first supplier of that energy and this demand surge is encouraging its growth of extra energy vegetation.

The way in which state-regulated utilities work is that they’ve a type of pre-planned revenue margin on new investments someplace round 10%. The regulatory our bodies will approve base charge will increase charged to prospects in order to fund the utility firm’s growth of latest energy sources.

In bizarre circumstances, the barrier to progress is that it may be troublesome to get the regulator’s approval to extend charges as a result of the regulators need to preserve energy accessible to customers. Nevertheless, in NOVA, there’s a clear scarcity of energy to service upcoming demand which is basically forcing the hand of regulators and making it simple for Dominion to get huge initiatives permitted.

Dominion already has the multi-billion greenback offshore wind venture off the coast of Virginia and in early April regulators permitted a brand new 764 MW photo voltaic growth. In keeping with an S&P International abstract, the approval got here with a big base charge improve.

“The brand new photo voltaic initiatives are anticipated so as to add roughly $1.54 to the typical residential buyer’s month-to-month invoice, Dominion stated”

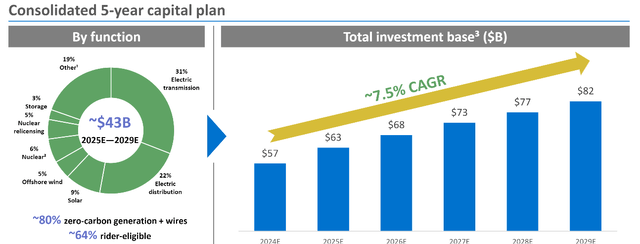

Dominion has an enormous capital funding pipeline summing to $43B over the subsequent 5 years which is able to practically double their funding base.

Dominion

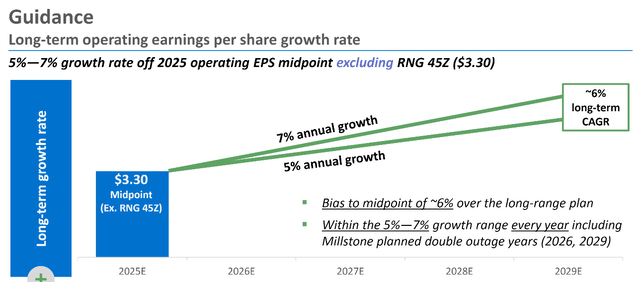

Because of the regular revenue margins of the trade, extra investments imply extra income. This capital outlay paves the best way for Dominion’s guided annual earnings progress charge of 5%-7%.

D

Dominion inventory valuation

At $48.68 Dominion is buying and selling at 14.75X guided earnings.

It trades roughly according to friends on different valuation metrics:

- Dominion money circulate multiple- 6.9X vs. friends at 7.7X.

- Dominion EV/EBITDA is 12.49X vs. friends at 11.57X.

Fourth quarter outcomes

I feel the market could have been dissatisfied within the 4Q23 headline earnings with a web earnings of $0.30 per share in comparison with $0.39 within the prior 12 months interval. Nevertheless, there have been important 1 time components distorting the end result.

Earnings from persevering with operations removes these one-time objects and confirmed important year-over-year progress coming in at $0.39 in comparison with $0.24 within the prior 12 months.

The quarterly numbers are lumpy so that they shouldn’t be straight-lined or extrapolated, however I do imagine the corporate’s reorganization is taking them in the fitting path.

Dangers to thesis

Being primarily within the utility enterprise, Dominion does probably not have competitors danger however as a substitute faces regulatory danger and danger of inner failure. Listed here are a couple of key issues that might go flawed.

1) Energy technology amenities fail to generate the facility for which they have been underwritten. In cases of facility injury or different failure, the corporate must carry out costly repairs or construct substitute energy in order to serve prospects. Normally, the corporate would request a charge improve to pay for the capital funding however this brings us to danger #2:2) Regulators reviewing charge instances can typically decline. There’s a high-quality stability during which regulators know they should permit utilities to be worthwhile in order to maintain the lights on, but in addition don’t need them to gouge prospects.

3) Energy reliability: As D strikes extra into photo voltaic and wind a bit extra variance to energy output is launched. These types of technology can produce fairly a little bit of energy, but in addition have surprising variance as ranges of wind and solar fluctuate. Dominion might want to stability these types of electrical energy with on-demand peaking vegetation to forestall shortages.

Dividend – flat for now

Regardless of the historical past of a dividend lower, the dividend appears fairly safe to me going ahead. That stated, I do not suppose it’ll develop a lot both.

Dominion’s dividend will doubtless be flat for some time as the corporate is focusing on a payout ratio within the 60s. Because the payout ratio is presently larger than that, they are going to doubtless wait to develop the dividend till the correct ratio is achieved. After that point, I think dividends would develop proportionally with earnings.

Ahead anticipated return – 11% yearly assuming flat a number of

A 6% ahead progress charge just isn’t all that unusual, however it’s not typically seen together with a 5.4% dividend yield. Normally, an organization must reinvest its cashflows to generate that a lot progress sustainably, however as a result of D is servicing the NOVA market which has a lot demand for further electrical energy, the expansion is ample in magnitude that even when funded by outdoors capital (fairness and debt) it could nonetheless end in a roughly 6% progress charge.

The 6% earnings per share progress in tandem with a 5.4% dividend yield would end in buyers getting an 11.4% annual return if the corporate continues to commerce on the identical a number of.

Under no circumstances is that this a homerun kind of inventory, however the mixture of worth and progress makes me suppose it’ll outperform the market. Traditionally talking, the market returns about 8% yearly so the 11.4% estimated primarily based on Dominion’s dividend and progress charge represents further return. I additionally imagine Dominion is barely under common danger for fairness provided that it’s an investment-grade, large-cap utility.

General, I feel that could be a nice deal and it makes for a pleasant addition to my portfolio.