The digital infrastructure sector’s progress has been fueled by the hyperscalers in recent times. The fast evolution of synthetic intelligence and the metaverse is about to drive this “zeitgeist” sector to new heights.

The emergence of generative synthetic intelligence (gen AI) and the metaverse is driving an explosion in demand for digital infrastructure.

The previous decade has already seen unprecedented ranges of funding in digital infrastructure on account of rising smartphone penetration, business digitalization and the rise of cloud computing, however the fast evolution of AI expertise, machine studying and the metaverse is propelling demand for information and computing energy to even better heights.

Powering these transformative applied sciences would require substantial funding within the information facilities and networks that ship the info and connectivity that AI and the metaverse would require to operate.

Hyperscalers

The first customers of knowledge heart capability and the principle drivers of demand are hyperscalers, a gaggle of enormous firms (together with the likes of Amazon Internet Companies (AWS), Microsoft Azure, IBM Cloud and Google Cloud) that present shoppers with computing energy, storage and software program structure that permits them to scale up capability throughout a number of servers and networks to fulfill the calls for positioned on software program and expertise methods at explicit instances.

In keeping with Jones Lang LaSalle, there can be greater than 1,000 hyperscaler information heart websites in operation by the tip of 2024, up from solely 500 5 years in the past. This can see the hyperscale information market develop at a CAGR of 20 p.c from 2021 to 2026.

These hyperscalers have more and more turn out to be the business’s focus, with builders, operators and traders setting up more and more massive information heart campuses. This in flip pushes demand for connectivity by means of fiber and towers.

Sustained funding from each hyperscalers and colocation builders in new information heart capability and the associated digital infrastructure can be important for assembly the surplus demand that may come from AI and the metaverse.

Market drivers: Defining the metaverse and AI

And whereas AI has turn out to be extra accessible and moved into the mainstream with the generative AI growth, firms are but to completely grasp what these applied sciences imply for doing enterprise, their progress and disruptive impression has nonetheless made investing in AI and the metaverse a business and strategic necessity for organizations.

The metaverse and the following evolution of the web

The metaverse, for instance, remains to be a broadly outlined idea that may imply various things to totally different folks. However though the metaverse has but to be exactly outlined, it’s influencing shopper conduct and company technique.

In essence, the metaverse and the following evolution of the web, and applied sciences that can be utilized to harness digital actuality and augmented actuality to construct digital worlds and facilitate frictionless interplay between digital and bodily areas.

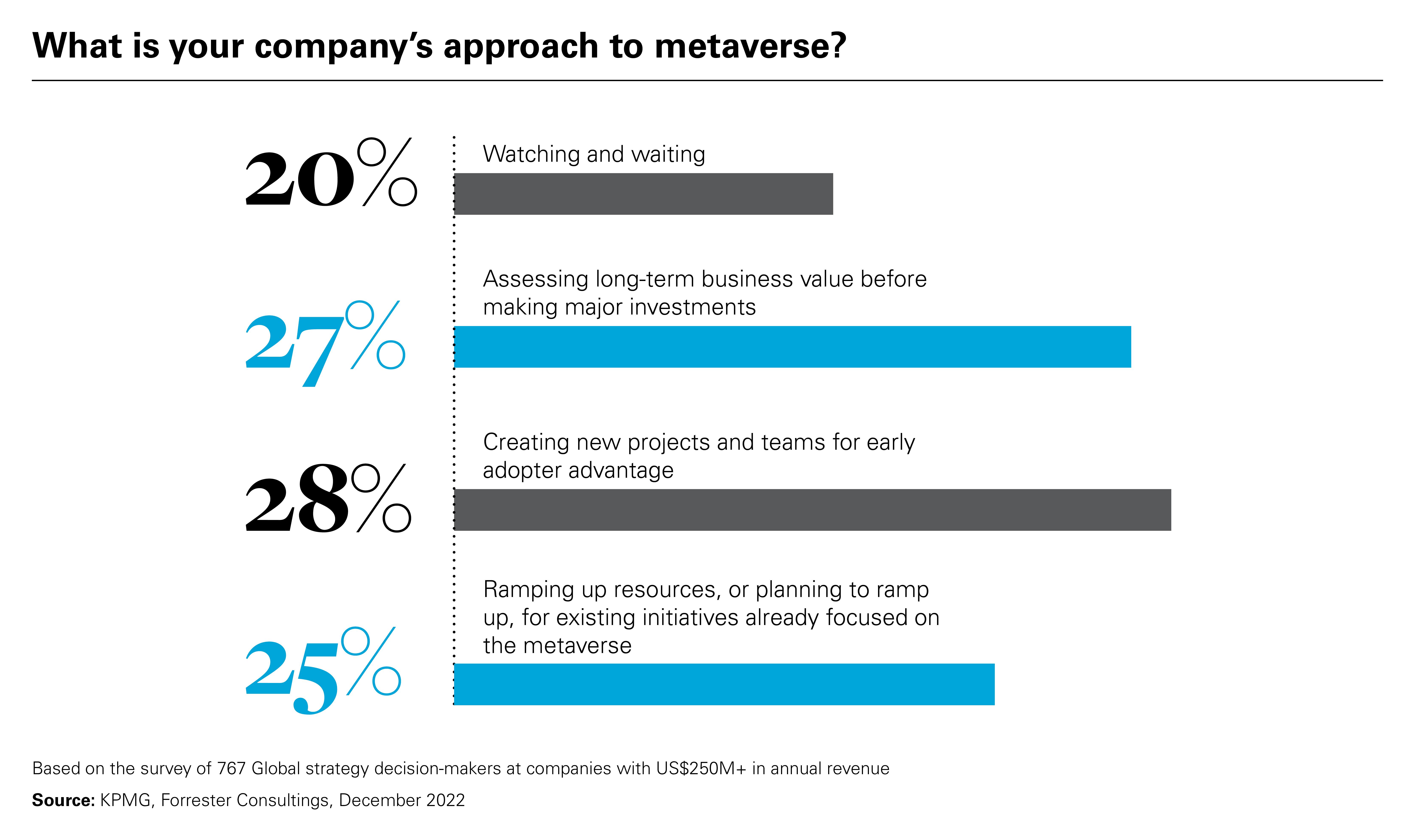

View full image: What is your company’s approach to metaverse? (PDF)

View full image: What is your company’s approach to metaverse? (PDF)

A KPMG survey of expertise executives confirmed that 60 p.c of respondents consider the metaverse can improve income and decrease working prices as transactions shift from the bodily to the digital. McKinsey, in the meantime, estimates that the metaverse may generate as much as US$5 trillion of worth by 2030.

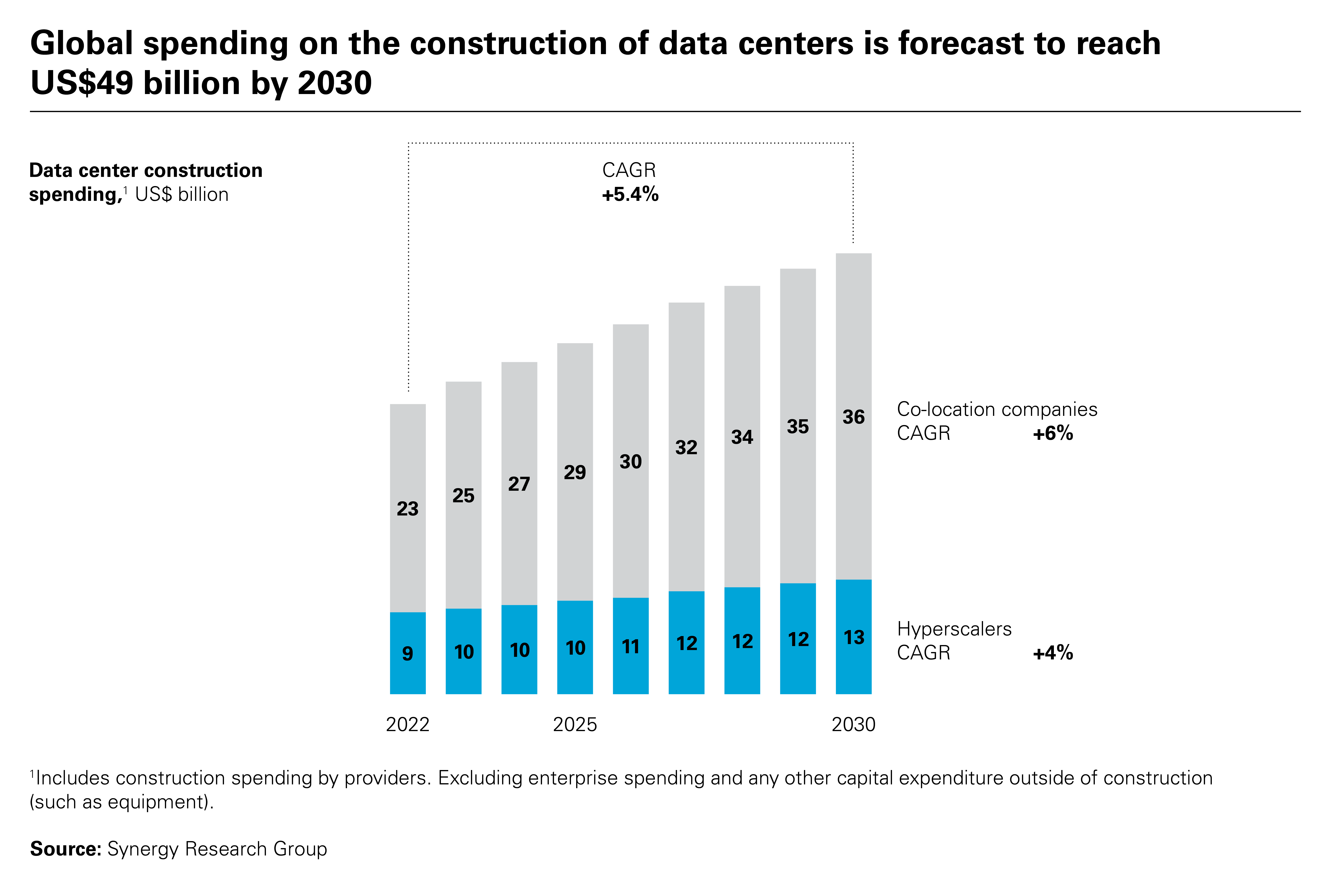

View full image: Global spending on the construction of data centers is forecast to reach US$49 billion by 2030 (PDF)

View full image: Global spending on the construction of data centers is forecast to reach US$49 billion by 2030 (PDF) Enterprise adoption of AI (the capability for a pc to execute duties that usually require human intelligence and judgment) has additionally surged, quickly gaining traction within the operations of industries throughout the board in recent times.

The fast progress and adoption of AI expertise in recent times is only the start

In keeping with DemandSage analysis, for instance, there are greater than 4.2 billion digital assistants resembling Siri, Alexa and Google now in use, with greater than 50 p.c of customers utilizing these instruments to seek out native companies, whereas procuring utilizing digital assistant voice search is about to ship worth of US$40 billion. Within the prescribed drugs sector, Wellcome Belief analysis reveals that AI may have a transformative impression on drug discovery pipelines, delivering time and price financial savings of between 25 p.c and 50 p.c; and within the wealth administration business, asset managers have constructed proprietary AI-powered instruments that fund managers are counting on to benchmark portfolio firm efficiency and supply potential deal targets.

The fast progress and adoption of AI expertise in recent times is only the start. In keeping with the Worldwide Knowledge Company (IDC), annual world spending on AI software program, {hardware} and providers is forecast to develop at a compound annual progress price (CAGR) of 27 p.c over the five-year interval to 2026, when it’ll exceed US$300 billion.

Challenges to be navigated

The necessity for digital infrastructure has ensured that capital has continued to circulate into the sector, shielding builders and traders from macro-economic dislocation.

There are nevertheless challenges to be navigated:

- Excessive margin developments of business-critical infrastructure expose operators and builders to doubtlessly materials liabilities. Authorized obligations, significantly within the context of growth and providers, will have to be understood and calibrated to make sure that tasks are each manageable from a company governance perspective and acceptable to the lending and funding group.

- Builders’ contractual obligations are beneath pressure. Inflationary pressures and provide chain disruption have impacted new information heart development and delayed tasks from coming on-line. In keeping with its most up-to-date Knowledge Centre Value Index, infrastructure consultancy Turner & Townsend discovered that 95 p.c of knowledge heart stakeholders had been experiencing delays because of materials shortages, with wait instances for some tools extending to 12 weeks or extra. Delays have pushed tasks over finances, including to the fee pressures coming from rising commodity and labor costs. These are more likely to result in rising developer default if authorized documentation is just not fastidiously negotiated.

- Environmental regulation and local weather change pressures can’t be ignored. Knowledge facilities are extremely power-consumptive, with some hyperscaler websites utilizing as a lot energy as 80,000 households, in line with McKinsey. McKinsey evaluation additionally reveals that new laptop chips and extra highly effective computer systems have seen common information heart energy densities greater than doubling in the course of the previous 5 to 6 years. Authorities insurance policies to cut back carbon emissions to net-zero have seen regulators pay nearer consideration to information facilities’ power utilization. An replace to the EU’s Power Effectivity Directive, for instance, would require information facilities of 500 kw or greater to report on power utilization and emissions from Might 2024. Andrew Jay, Head of Knowledge Centre Options, EMEA for CBRE, agrees that this can be a problem that the sector might want to confront, “New and current Buyers will proceed to concentrate on the ESG credentials of those services and this scrutiny will turn out to be more and more extra essential because the power consumed by information centres turns into extra vital when put next with different home usages.” Authorized documentation on this sector might want to transfer within the path of transparency with respect to consumption and efficiencies to maintain step with this agenda.

- Anti-trust and competitors. The sector has discovered itself on the radar of competitors and antitrust authorities too, with the UK’s Competitors and Markets Authority (CMA) launching a probe into the chance to competitors within the UK information heart ecosystem on account of the dominant market share held by a handful of hyperscaler gamers. Regulators worry {that a} lack of competitors available in the market could make it tough and expensive for patrons to change suppliers. M&A exercise was sluggish in 2023 and these regulatory pressures are more likely to turn out to be extra evident as transaction volumes start to select up as anticipated by many.

- Financing constructions. The rising affect of hyperscalers can be reshaping the way in which information facilities and digital infrastructure are financed. Non-public funding, for instance, has been a key supply of capital for information heart growth, with McKinsey noting that non-public fairness’s share of mixture information heart deal worth elevated from 42 p.c between 2015 and 2018, to greater than 90 p.c by 2022. These dynamics, nevertheless, are shifting, as hyperscalers turn out to be extra influential and leverage their positions as anchor prospects to barter extra favorable contracts and leasing phrases, squeezing the margins of co-location information heart operators within the course of. This has tempered flows of personal capital, with traders additionally shifting cautiously for expensive information heart belongings in a risky deal market that has been hampered by rising rates of interest. With debt markets throughout the board additionally tightening on account of rising charges, digital infrastructure operators and traders could must discover new constructions and choices to finance roll-out of further capability within the quick to medium time period.

Metaverse may generate as much as US4% trillion of worth by 2030

Supply: McKinsey

Digital infrastructure now presents traders publicity to belongings with sturdy market positions and excessive ranges of repeat income

Digital infrastructure: The muse for AI and the metaverse

There’s a necessity for extra digital infrastructure to help the anticipated progress in AI and the metaverse.

Digital infrastructure encompasses all of the underlying frameworks that enable digital instruments to operate, together with {hardware}, software program, community connectivity and information facilities. It’s the basis of all of the digital providers, web instruments, connectivity and cloud computing functions which have turn out to be important for contemporary economies.

AI and the metaverse utility require significantly massive information sources and computing energy to operate, and as uptake continues to speed up, will place ever-greater masses on digital infrastructure capability. In keeping with Gartner analysis, generative AI accounted for lower than 1 p.c of knowledge produced in 2021 however will swallow up 10 p.c of capability by the tip of 2025–and proceed to develop in subsequent years. Intel, in the meantime, has estimated {that a} 1,000x improve to present computing capability can be required if the metaverse is to appreciate its full potential.

Andrew Jay is obvious on the chance for the business, “The AI growth is about to drive one other wave of change and growth for European information infrastructure. A lot of the brand new capability can be absorbed by the hyperscale operators, however vital alternatives exist for colocation distributors to develop new purpose-built services. The pace and scale of the expansion is resulting in a brand new entrance of capital companions who’re wanting to be on the forefront of the sector and seize the ever-expanding take-up in EMEA.”

Demand for information and computing energy is already outstripping provide, with rising applied sciences fueling additional urge for food. Regardless of rising world rates of interest, inflationary pressures and a weakening macro-economic backdrop, long-term demand drivers have positioned digital infrastructure as a fast-growing, resilient asset class for traders, builders, operators and lenders.